From factsheet to reality: Bridging the investment performance gap

In investments, it is very seldom that the portfolio manager and the investor experience the same return figures. We’re going to explore two ways to measure performance and unpack where the portfolio manager’s responsibility starts and ends.

Spoiler: investor composure is only part of the story.

Two windows into the industry

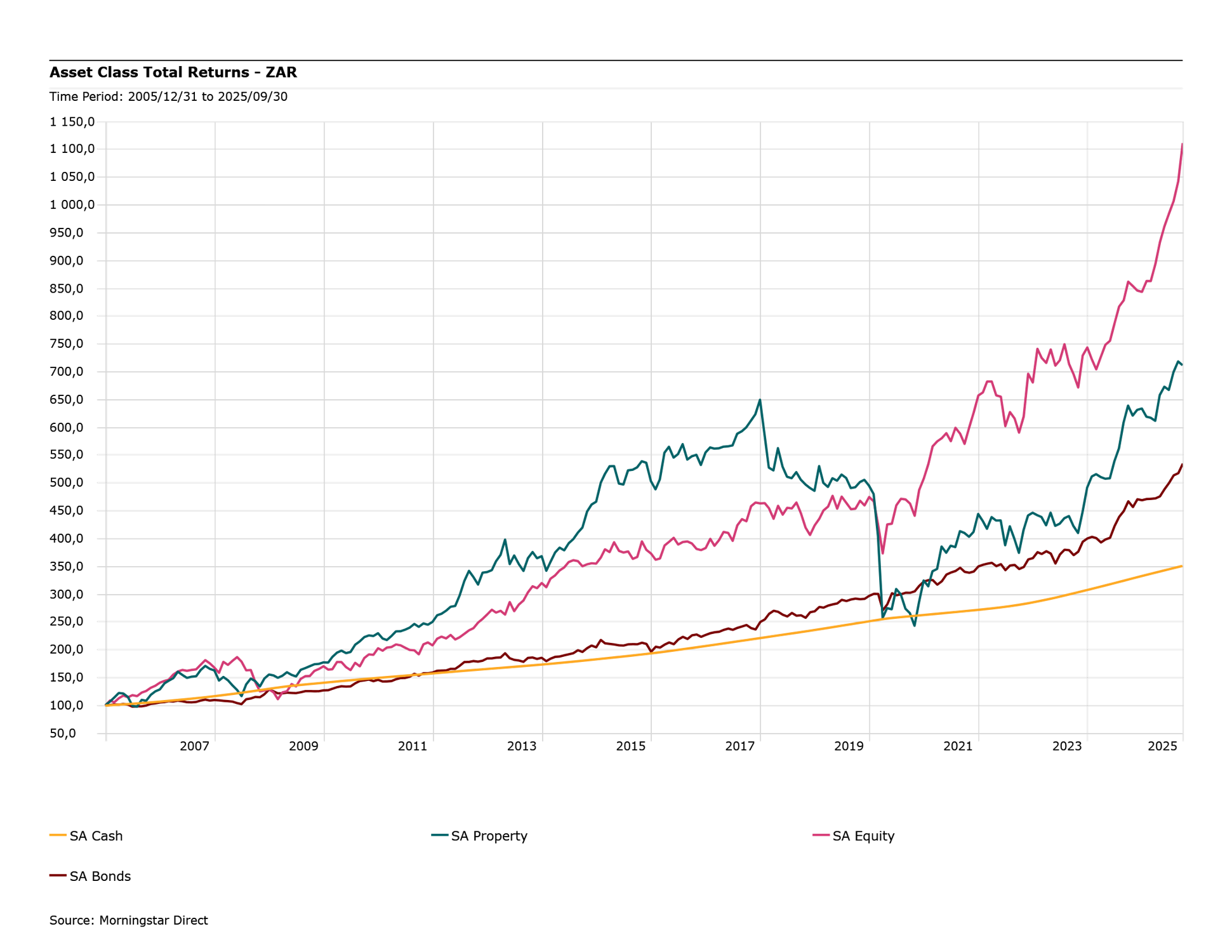

Fund performance can be measured in two main ways, and each tells a different story. The time-weighted return (TWR) is the figure you see on a fund’s factsheet; it measures how the investment itself performed over time, ignoring any money flowing in or out. In essence, TWR answers, ”How did the fund do, if we assume a fixed investment throughout?”. The money-weighted return (MWR), by contrast, accounts for the timing and size of contributions or withdrawals, reflecting how an investor in the fund performed. This is aligned to the return on the investor’s statement. Clearly these are not the same.

So why does the industry have two measures of performance for the same fund?

Traditionally you’ll be told to think of TWR as the fund manager’s scorecard as it isolates their skill by removing the impact of investor cash flows (I’m going to challenge this assertion). MWR, on the other hand, shows the investor’s experience; it is the result of not only the fund’s performance, but also the investors’ money-weight exposure to the fund.

In a perfectly steady world with no cash flows, TWR and MWR would be identical. But in the real world, they often diverge whenever investors pour money in or withdraw money out at various times.

The “Behaviour Gap”: When investors earn less than the fund

Investors often find that their personal returns (MWR) are lower than the fund’s published returns (TWR). This shortfall is commonly called the “behaviour gap,” defined as “the difference in return between what the factsheet shows and what our investment actions delivered”. Why does this gap happen? Well, a foundational principle of investment management is a concept of “the rational investor”, which we don’t believe exists, in large part because real people don’t invest and forget, we get excited and fearful.

Studies by Morningstar (their annual ‘Mind the Gap’ study1) have found a persistent pattern: investors tend to buy high and sell low, chasing performance on the way up and panic-selling on the way down. Over time, this behaviour can cause investors to consistently underperform the very funds they invest in. It may only be a percentage point or so each year, but that small annual drag adds up; over 30 years it could mean a retirement nest egg that is 40% smaller.

There are a few serial offenders that cause investors to behave this way, but volatile funds such as thematic investments lead the way. The exciting storytelling of clean energy, or artificial intelligence, are often the highest-flying funds on paper (TWR) but can deliver the poorest investor experience (MWR) in practice. When hype unwinds: A real-world example Let’s look at a recent example of the behaviour gap in action. The iShares Global Clean Energy ETF became a star performer in 2020 with a 140% return that year. Excited by this success and the headlines surrounding it, investors piled into the fund, doubling the fund size by January 2021. But the hype didn’t last, and the theme rolled over. Assessing the fund over a five-year period reveals a handsome factsheet return was +17% per annum (TWR), however, the average investor in that ETF actually lost about 3% per year (MWR).

That’s a staggering ~20% performance gap, and the flag that is common across most experiences such as this one is a compelling theme or narrative that can entice investors at exactly the wrong time. The hype fades and investor allocations, and often returns, unwind.

Why do we not learn our lesson? Brandon Zietsman explains how our relationship with an uncertain future often drives us to seek comfort in stories and trends. Author Morgan Housel states that we “crave certainty and are attracted to complexity. Good stories persuade us far more than facts”.

Who bears responsibility for the gap?

Given this gap, a crucial question arises: who is accountable for it? Traditional thinking might say the investor is responsible for their timing decisions. However, an investor-centric solution (like that of PortfolioMetrix) suggests shared responsibility. If a fund’s design or the way it’s promoted encourages counterproductive behaviour, the manager should arguably bear some responsibility for the outcome. For example, a fund that aggressively touts its exceptional past returns might inadvertently lead people to buy in at peaks. In such cases, the manager’s scorecard shouldn’t just consider TWR, but also how investors actually fared via MWR (a customer survey so to speak). Did the majority of investors in the fund capture those high returns, or did they suffer a large behaviour gap? A truly skilled manager (or strategy) would ideally produce good TWR and help investors stay the course to realise those returns. The factsheet and the investor’s statement would be close cousins rather than distant strangers.

The PortfolioMetrix approach to bridging the gap

Historically the burden of reducing the behaviour gap has been passed to the adviser like a hot potato, or simply blaming bad investor composure. We believe the answer lies in those traditional practices, and in better portfolio design. On the portfolio side, it means constructing diversified, robust portfolios that investors can live with through thick and thin. Avoiding single-factor risks, and identifying the investor’s Financial Personality, mapping them across into their composure zone, and ensuring they invest in a solution (not a product) that best suits them and their financial goals. These concepts are in our DNA at PortfolioMetrix. We aim to engender trust by building strategies that don’t rely on chasing the latest theme or taking extreme bets. A well-diversified, risk-managed portfolio may not shoot the lights out in any one year, but it also won’t inspire the kind of boom-bust behaviour that leads to large behaviour gaps.

We aim to compound consistency into long-term outperformance, an investment strategy that complements the adviser’s value-add, builds trust, and helps us all sleep well at night.