Investors behaving badly: a cheat sheet to narrowing the behaviour gap

Emotions define us as humans, but it also costs investors over 1% per year according to Morningstar. Advisers who pro-actively engage in behavioural coaching with their clients will tangibly add value to the investors experience. Perhaps you may also find that whilst markets are cyclical, your business doesn’t necessarily need to be.

An advised client stands to benefit the most

Our emotions are a differentiating factor from robots, artificial intelligence, and behaving like the “rational investor”. The price paid for this individuality, observed within our investments, however, is the behaviour gap; the difference in return between what the factsheet shows, and what our investment actions delivered.

Traditional investment theory unfortunately doesn’t accommodate all too much of this true human behaviour into our many models, instead it assumes the idea that investors behave rationally. However, in the heat of “battle” humans are driven by emotions and cognitive biases. In fact, Vanguard estimates the value an adviser can add to their client’s journey is nearly 2% p.a. (through behavioural coaching).

Key target areas for behavioural coaching, evidence from across the globe

Morningstar has recently written two reports analysing the behaviour gap. They used their vast database of fund returns, and fund flows, to determine when and where investor behaviour adds value to their net result. Their conclusions are not all too surprising:

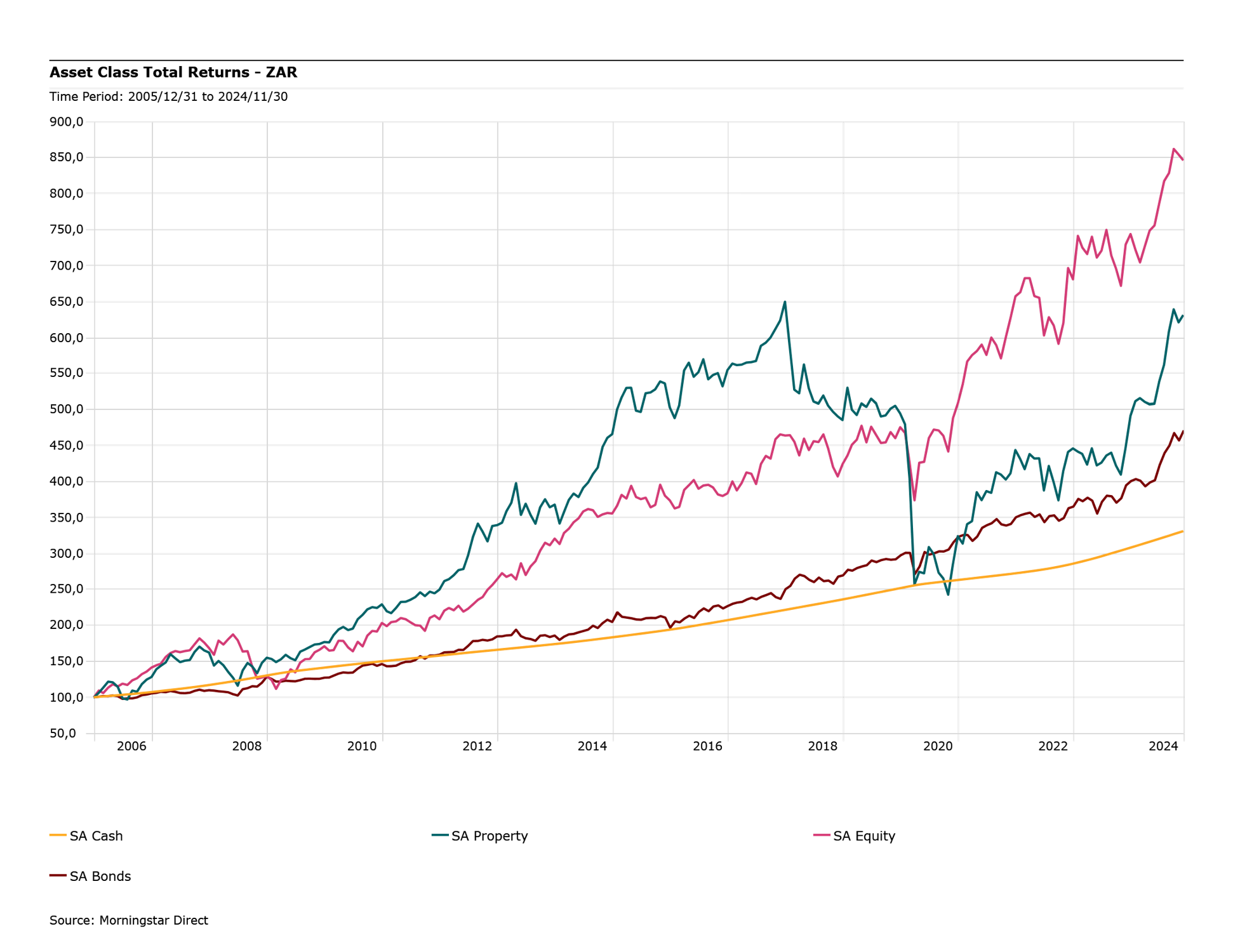

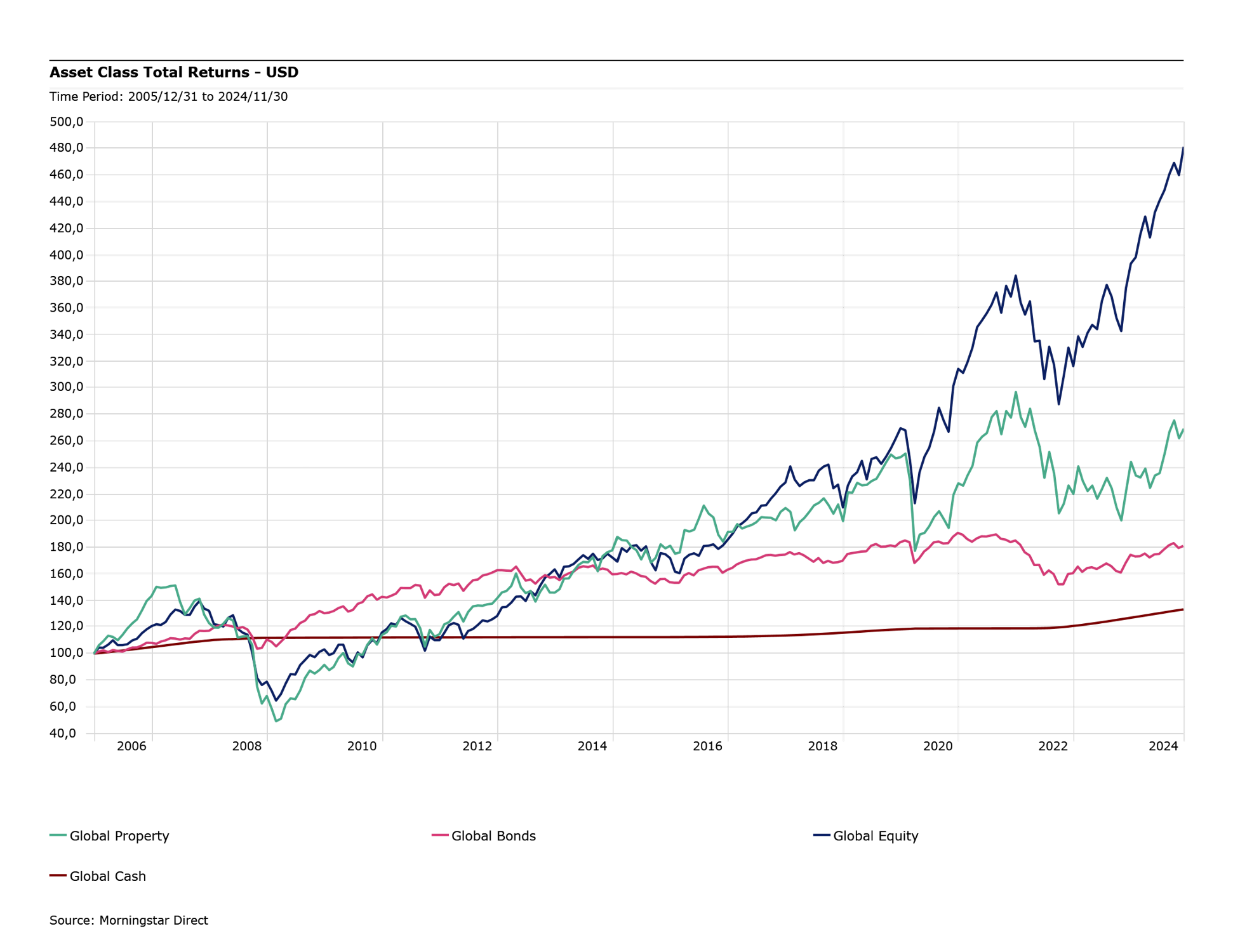

Investors consistently behave badly: across their 10-year study, investor behaviour consistently detracted from a buy-and-hold strategy. This was greatest during big market drawdowns such as 2020 and 2022.

Performance is more tangible than risk-management: The top performing funds (time-weighted returns) attracted the most flows, but also presented the greatest behaviour gap as performance often turned after attracting the industry’s attention. This performance chasing, or misallocation of capital, by investors is based on exciting thematics rather than a sound investment process.

Diversified portfolios narrow the behaviour gap: Multi-Asset class funds demonstrated the smallest behaviour gap of all categories analysed. The widest gap was observed in the most volatile and narrow-focused strategies such as sector-specific equity, value style, and other storied investment themes.

Investor trust is fragile: Active strategies present a larger behaviour gap than passive strategies do. This is a nuanced topic but interestingly when controlled for fees the report does not observe a discernible behaviour gap, perhaps speaking more to the fragility of investor trust.

The behaviour gap in action

Some of the most interesting examples of the behaviour gap include the iShares Clean Energy ETF which after an exceptional 140% return in 2020 saw its assets double to over $6bn by January the next year. In the five-year period under review the annualised factsheet return was 17% per annum, however the average investor in the ETF would have observed -3% per annum. A behaviour gap of 20%!

Similarly, other narrow-mandated strategies such as the JP Morgan Pacific Technology fund and the iShares Barclays Cap USD Asia High Yield Bond ETF exposed investor misbehaviour to the extent of 17% and 12% respectively.

Morgan Housel spoke directly to why these investments appeal to investors when he wrote, “We crave certainty and are attracted to complexity. Good stories persuade us far more than facts”. We cover this topic from an adviser’s perspective in this article. As Vanguard stated in their whitepaper in which they attempt to quantify adviser’s alpha, “The markets are uncertain and cyclical – but your practice doesn’t have to be”.

The journey matters, and we know it

These concepts are in our DNA at PortfolioMetrix. When building client portfolios, we look to engender investor trust through portfolio construction. Pairing behavioural coaching and broader financial advice with this investment approach is going to drive a far smoother experience for the investor as they navigate the various stages of their investment journey.